Download PDF:Tax Free Retirement, Income for life guide

Download PDF:Tax Free Retirement, Income for life guideby James Burns

One hundred years ago only one in four Americans lived past the age of sixty-five. Today, three in four people surpass sixty-five. We expect to live longer and with the tremendous advances in medical science, people living into their eighties and nineties is going to become commonplace.

Emerging generations are going to need a more effective financial strategy due to this increase in life expectancy, not to mention the fact that costs are rising while the value of the dollar is shrinking worldwide.

The two previous generations, the immigrants and the baby boomers, had a different way of looking at life. They were taught four principals that were supposed to create success and happiness if followed correctly:

1. You get a college education

2. You get a job,

3. Get married and start a family,

4. Buy a house and pay it off as soon as you can, so you can be secure in your retirement.

The evidence is now clear that this formula no longer works in creating the kind of wealth the current generation of workers will need in retirement. The US Department of Health and Human Services says that 36% percent of sixty-five year olds are still working, 54% are dependent (require family or government assistance), five percent are deceased, 4% are financially dependent (with at least $3,000 per month to live on) and one percent are wealthy.

We know because of our aging population that providing Social Security to future retirees will require higher taxes or reduced benefits. As we‟ve discussed throughout this book, the traditional retirement formula is going to leave you broke. The wide use of mutual funds tied to market volatility that contain both disclosed and concealed fees is just not reliable.

If you consider John Bogle‟s insightful examination of three hundred fifty-five funds over a thirty-five-year period,1 there is no question that most mutual funds are not where you want your retirement dollars. Even if you find a good index fund, it may be so overly saturated that getting ahead will require some form of miracle.

The ideal long term savings vehicles have a few common characteristics:

1. Performs Well in a less robust market

2. Reduces or eliminates risk

3. Tax Efficient

4. Low Expenses

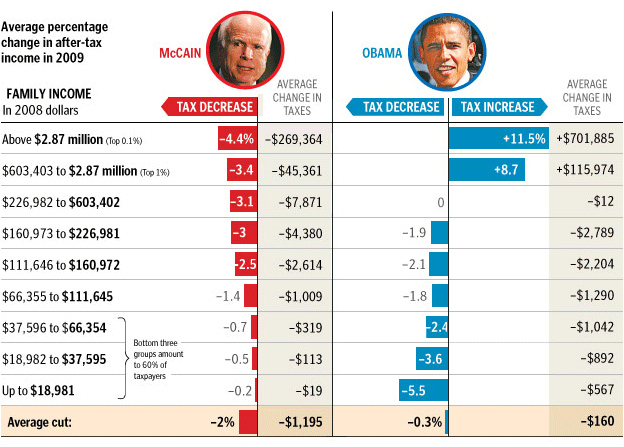

The future of our tax scheme is uncertain but the Washington Post provided the following comparison of the two presidential candidates. 2(article)

At the time of this writing, you can see it is prudent to consider total tax-free income in your retirement years. I make no proposal for either candidate but the messages are clear based on the comparison that Senator Obama will increase taxes across the board. Senator McCain will likely have to do more and most tax prognosticators agree that the entire marginal tax rate has to shift upward to meet the demand in debt, benefits to Boomers and the war on terror including the Homeland Security aspect of it.

The American Dream of being able to ascend your class is being foreclosed on and the recipe for even more difficult times are ahead, if we have the one plan that threatens the break-out upper middle class and makes them pay everything. You‟ll absolutely need to have a tax-free (4) income strategy in your retirement years.

Even if this never came to pass, the idea of deferral just does not do justices because most Americans retire in a higher tax bracket if they‟ve been successful and if the entire table shifts. Anything you have in a deferred plan will be taxed at the ordinary income which means, you‟re deferral will be lost within 2 years typically. Just ask yourself this question, does it make more sense to be taxed on the seed or the harvest?‟ If you said the harvest, you‟re right. Think about it, a seed is much smaller and that would be the time to be taxes; and a harvest is of plenty which means much more tax eating away at it.

There is also a Solo Roth 401(k) which is a 401(k) for an individual that beats the Roth IRA five times over. Unlike the previous opportunity for retirement savings (the Roth IRA), the new Solo Roth 401(k) will allow an individual or married couple who own their own business, to sock away up to $98,000 per year for retirement. Of this amount, $40,000 can be composed of after-tax Roth elective contributions (provided the individual, and their spouse, if applicable) are both over fifty. So now, for the first time in history, a retirement saver can put up to $20,000 in a retirement plan that can grow annually into a retirement plan that can grow tax-free for their lifetime.

Not only is this amount five times greater than what can still be put into a Roth IRA ($4,000 limit, plus a $500 catch up if older than 50), but there is no cap on the amount of income an individual can earn before he or she becomes ineligible to contribute. So, while one is (5) restricted from contributing to a Roth IRA when he or she earns more than $110,000 ($160,000, if married filing jointly), no such restriction exists for the elective Solo Roth contributions!

In addition, with the Solo Roth 401(k), you can invest in two types of investments (“S” corporation stock and life insurance) that are restricted for Roth or traditional IRAs. Moreover, unlike your IRA where you cannot take out a loan, you can personally borrow up to $50,000 or 50% (whichever ever is less) from your Solo Roth 401(k).3 That provides a cash flow opportunity that a Roth IRA cannot provide.

Heres an example of how it works: say you earn $100,000 in 2007 from your sole proprietorship. Your maximum solo 401(k) contribution would be $35,500 (that is, the $15,500 maximum salary deferral contribution plus 20% of the $100,000 you earned). With traditional self-employed retirement plans, your maximum contribution in this case would be $20,000 dollars instead, which is much less.

In addition, the contribution limits for a Solo Roth 401(k) are much higher than the $4,000 Roth IRA contribution limit. So if you‟re self-employed or a business owner with no employees other than your spouse, a solo Roth 401(k) is a great way to sock away more money into a Roth and reap the benefit of tax-free growth on your earnings.5

5. Id at http://www.penscotrust.com/education/solo_roth_401k_and_solo_401k.asp

6. Money Girl – http://moneygirl.quickanddirtytips.com/solo-401k.aspx

With traditional IRA’s and Roth IRA’s, any income or capital gains on debt-financed property is taxed at the trust tax rate (generally 35%) to the extent that debt supports the generation of the income. This is a very important benefit to real estate investors who are in the position to be eligible to form a Solo 401(k). Unlike investing outside of a retirement plan, where taxes apply to net income and any gains generated by debt financing, unless they are sheltered through a 1031 exchange, 401(k) plans are exempt.

The secondary benefit is the avoidance of having to go through the 1031 process and its expense. For example, you could literally buy a house in the morning with $100 down and flip the purchase contract in the afternoon, without paying any tax on the gains. The gains would

be tax-deferred thereafter, if they had been funded by the tax-deferred components of the Solo 401(k), or tax-free if funded by the elective Roth component.

In conclusion, we have the opportunity to perform well in a less robust market because you can fund your solo-401(k) or self-directed Roth IRA with real estate and other assets that are not connected to the market. You cannot reduce or limit risk with this vehicle because there are no safety measures built in like the insurance chassis. It is definitely tax efficient because you‟ll pay no taxes in retirement by having a ROTH where you’ve paid your tax up front on the seed rather than the harvest. Finally, the expenses can be reduced by creating and LLC that does most of your investing, but you are also disconnected from the usual market fees by using real estate and debt related investment assets to fund this plan.

The Two Major Applications of Life Insurance

There are two main uses for life insurance from a goal setting perspective. The first is succession capital, which is what people generally hear about in regards to how it will protect their families or estate in case the breadwinner departs. Its the money your family or estate receives in the case of your death. However, you also have lifestyle capital, which is designed to create future tax-free cash flows as a supplemental retirement income. Unlike your pension plan, which will be taxed as ordinary income at your tax bracket; this income can be distributed tax-

free.

If you are not thinking about your net “spendable” income (NSI) in your retirement years, then youre not developing a winning wealth plan. You need to know exactly how much youll need to maintain your lifestyle when you retire. Youll also need to factor in the costs of increasing medical needs.

Using other people’s money (OPM) with the intent of realizing a financial gain is a financial concept that has been practiced by real estate developers, investors, business owners and entrepreneurs for centuries. Today, this concept is being utilized to purchase life insurance, and has raised the eyebrows of insurance promoters and financial professionals alike. Does this concept offer economic substance or is it just another sales tool to sell life insurance?

Life insurance is an important part of any high net worth individual‟s financial picture. Since adequate life insurance usually requires significant premium payments, the premium financing strategy can be an effective solution for clients who do not want to liquidate assets to fund their life insurance premiums.

Premium financing is a method of funding the purchase of life insurance for those individuals who have significant assets, but do not have or want to use liquid capital to pay the premium on a life insurance policy. By borrowing the money to pay the life insurance premiums with a loan, the insured individual frees up capital that can be used more efficiently. The use of premium financing may lower out-of-pocket costs and potential gift taxes.

Im often asked the difference between qualified and non-qualified plans, and I think it is important to explain it by example since most tax preparers look at the pretax dollar aspect of a qualified plan. My mantra is it is better to be taxed on the seed rather than the harvest”, which runs contrary to the conventional tax preparer way of thinking.

6. Andre Blaze, “Life Insurance Premium Financing—What to Look For.”

Qualified

Joe, age thirty-five, wishes to retire at age sixty-five; Joe is in the 30% tax bracket.

Joe deposits $30,000 per year for thirty years at 8% interest, equaling $3,398,496.

Joe receives a tax savings per year of $9,000, for a total tax savings of $270,000.

Joe would receive a “net” retirement income of $290,000 per year, assuming a 30% tax bracket.

His money would last for just 13 years.

Total taxes paid by Joe on his retirement income would be over $1,500,000.

Total net retirement income after taxes of $3,900,000.

Non-qualified

John, same age deposits $30,000 per year to the age of sixty-five, assuming an 8% return.

John receives NO tax savings on his deposits.

John receives a “net” retirement income of $290,500 per year to the age of one hundred plus.

John‟s total taxes paid on retirement income equal $0.

His total net retirement income after taxes is more than $10,000,000.

DIFFERENCE

Taxes saved on deposits are $270,000 on qualified plan. “0” on non-qualified plan.

Taxes paid on retirement income of over $1,500,000 on qualified plan and

$0 paid on non-qualified plan. That equals a tax savings of over $1,230,000.

Total net income paid of $3,900,000 on qualified plan, and $10,000,000 paid on non-qualified plan. That‟s a difference of $6,100,000.

Overall difference of $7,330,000.

The non-qualified plan has an initial death benefit of over $2,000,000 in case John was

to pass early. You’ll have to be the judge, but the smart approach to the money would be looking

at the end game. It truly is better to be taxed on the seed than the harvest. Perhaps the best

solution is to use both and spend down the least efficient dollars first. These are the qualified plan

dollars subject to ordinary income tax. Then use the non-taxable funds that are created with a

non-qualified strategy.

Many investors are unaware that cash value life insurance is the only investment tool that acts as a self-completing college funding, a supplemental retirement savings plan and can be creditor proof in some states. A great argument these days is that the cash value build up is the functional equivalent of a retirement plan garnering comparable protection. Fabulous feature include the ability to build-up and not count this cash value as an asset for the purpose of financial aid when your children head off to college.

Finally, by over funding a cash value life insurance policy, up to the modified endowment contract (MEC)7 guidelines, it can become “savings grade life insurance.” To further maximize the opportunity with life insurance in order to take advantage of the tax-free environment you overfund in relation to the death benefit.

7. A modified endowment contract is defined as any life insurance contract entered into on or after June 21, 1988, that meets the life insurance requirements of Code §7702; but which fails to meet a special seven-pay test or is received in exchange for a modified endowment contract [I.R.C. §7702A(a)].

Over funding is a strategy that focuses on accumulating cash in the policy rather than paying for the death benefit which is the payout to your loved one’s when you pass away. This approach leverages the highest policy premium that is allowed with the lowest life insurance death benefit so that your cash accumulation exceeds your policy net insurance costs over at least 10 years. There are fundamentally 4 steps to determining the combination of maximum premiums and minimum death benefits necessary to selecting the most leveraged indexed universal life policy:

First, determine the person‟s maximum premium commitment over a…

1. Minimum of ten years or more. The premium amount selected should be an amount that they can make regularly, whether it is a monthly or annual payment and does not strap their cash flow. Universal life insurance policies offer flexible premium payments; but to get the maximum leverage you have to stay on course with a premium payment.

2. Secondly, determine the minimum insurance face amount and payment commitment along with your age and gender to make sure the numbers work based on your particulars. Most insurance illustrations provide the actual premium amount limits that meet the internal revenue code minimum requirements.

3. Next, go over the internal rate of return (IRR) of the policy to ensure you‟ll be getting the full benefit of the tax-free accumulation versus what an ordinary investment would receive outside of this tax-free environment. Some agents illustrate way too high like 8% which is unrealistic. We usually do ours at 5.25% and still kick the pants off other investments.

4. Finally, you must pay close attention to the maximum premiums allowable under the Internal Revenue Code which is referred to as the seven-pay premium limitation. As long as the total premiums for any seven-year period are equal to or less than the maximum allowable premiums for the seven-pay test, you‟ll be able to access the cash values in the policy at any time, tax-free and relatively liquid.

In essence, a life insurance contract that fails to meet the seven-pay test will be classified as a modified endowment contract (MEC). The seven-pay test is not met if the accumulated amount paid at any time during the first seven years is more than the total of the net level

premiums that would normally have been paid on or before such time, if the contract provided for paid-up future benefits after payment of seven level annual premiums

8. IRC §7702A as part of the Technical and Miscellaneous Revenue Act of 1988 (TAMRA).

9. I.R.C.§7702A(b).

Accessing the savings

The reason you’re able to access your savings in the cash value tax-free is because it will be characterized as a loan. This is a so-called “wash loan” because the interest rate the borrower pays and the interest rate the insurer pays on the cash value are the same, so each rate “washes out” or equalizes the other.

For example, suppose the current rate the insurer is paying on the cash value account is 7% and the policy loan rate is 6%. With a wash loan, the 7% rate would be reduced to 6% to match the loan rate. Fixed, indexed, and wash are the three loan options offered by many carriers these days. The goal is to use leverage to create more wealth with the right insurance framework; and if it has a dynamic loan provision, you can make money on dollars that you’ve taken out taking advantage of arbitrage, which builds your cash flows. This can happen with certain insurance products that credit 140% of the S&P on borrowed cash values in the policy.

To illustrate, the loan interest rate is 5%, you get credited 140% of the S&P (up to a cap of 10%), which in this case creates 7% minus the 5% loan rate and you are left with a net result of 2% on money that is no longer in the policy. To understand this better, you should talk to a qualified professional planner.

10. If a loan is still outstanding when a policy is surrendered or allowed to lapse, the borrowed amount becomes taxable at that time to the extent the cash value exceeds the owner‟s basis in the contract. A policy loan is defined in subsection 148(9) as an amount advanced by an insurer to a policyholder in accordance with the terms and conditions of the life insurance policy. Although these advances are referred to as policy loans, they are actually advance payments of a policyholder’s entitlement under the policy.